From Middle East Conflict to Domestic Pressure: Kenya’s Export Economy Under Strain

While the country reels from the controversy surrounding the fuel scandal, the long-term effects of disruptions in the Middle East are already taking shape. Vellum Kenya’s “Not Our War, But Still Our Problem: Africa and the Middle East Crisis” highlights both the near-term and structural implications of the U.S.–Iran conflict on African economies.

Beyond energy, the article outlines that the crisis is driving a broader reconfiguration of global trade routes. Maritime disruptions in the Gulf have increased freight costs, delayed shipments and introduced new bottlenecks for African exports. At the same time, the supply of critical imports, especially fertilisers, has been constrained. This raises the risk of food insecurity across Africa, as fertiliser prices are expected to rise, partly because some components are oil-based, and global shipping rates remain elevated.

The real economic impact of the conflict is already evident in key revenue-generating sectors. According to a statement issued this Friday by the Kenya Tea Development Agency (KTDA), the conflict has already interfered with critical export routes, resulting in shipping delays and higher freight and insurance costs.

The agency further notes that rising fuel prices are expected to increase the cost of fertiliser in the coming months, exacerbating pressure on agricultural production and export competitiveness, with negative implications for tea farmers’ earnings.

Exposure of Kenya’s Export Economy to External Shocks

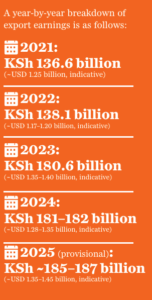

To contextualise the economic significance of Kenya’s export revenues, it is instructive to examine the export value of the country’s key commodities, using the example of the tea sector, which remains a primary foreign exchange earner.

This data would provide useful indication of the extent to which external shocks, including geopolitical disruptions and rising logistics costs, can transmit into macroeconomic pressures, sectoral earnings, and rural livelihoods.

According to the Kenya National Bureau of Statistics (KNBS) and industry data, tea exports generate approximately USD 1.2–1.5 billion annually, consistently positioning the sector among the country’s leading foreign exchange earners alongside horticulture and tourism. The trajectory shows relatively stable performance in 2021–2022, followed by a marked increase from 2023 onwards. Variations in USD values across the period largely reflect exchange rate movements and global price dynamics rather than structural changes in export volumes.

It is, however, important to note that this value is derived from countries whose access is directly affected by the conflict. Pakistan, for instance, is the largest market for Kenyan tea. It accounts for roughly a third of total exports and serves as the main price-setting destination for a significant share of auction volumes. The United Arab Emirates (UAE) also plays a strategic role as a regional re-export hub into the Middle East, alongside other notable destinations such as Saudi Arabia, Russia, Iran, India, and Yemen.

Collectively, these markets absorb the majority of Kenya’s tea exports, with Asia and the Middle East dominating the demand profile and creating a strong dependence on maritime trade routes through the Red Sea, Suez Canal, and wider Indian Ocean shipping network.

This underscores the sector’s heavy exposure to geopolitical disruptions with immediate implications for macroeconomic stability, sectoral earnings, and rural incomes.

Policy & Regulatory Stabilisation Support

Granted, President Ruto’s recently restructured National Economic and Social Council (NESC), with the vision of transforming Kenya and positioning it as a net exporter rather than a net importer, there is a clear need to cushion sensitive, export-oriented and high-revenue sectors against external shocks.

This policy direction is already reflected in Kenya’s responsiveness to global volatility, as demonstrated through the VAT (Amendment) Act, 2026, which reduced VAT on critical and price-sensitive petroleum products from 16 to 8 per cent temporarily to cushion households and businesses from fuel price shocks linked to global geopolitical disruptions and supply constraints.

This approach is consistent with global practice, where governments have responded to fuel price shocks through temporary VAT reductions, excise duty cuts, and targeted subsidies to cushion households and protect productive sectors. Comparable measures have been implemented across Europe and Asia, including in Spain, Poland, Germany, and the Philippines, reflecting a shared policy response to external energy and geopolitical shocks.

Building on this foundation, similar adaptive policy approaches could be extended to protect strategic export and foreign exchange–generating sectors from sudden disruptions. This would help safeguard export competitiveness and reinforce the broader objective of transitioning Kenya toward a sustained net-export position.

In this context, the tea sector could also benefit from targeted reductions in the tax burden on tea production and exports, particularly through a review of levies and statutory deductions that cumulatively weigh on farmers’ earnings.

Tea remains one of the most heavily taxed agricultural value chains in Kenya. For example, smallholder farmers supplying factories under the Kenya Tea Development Agency system typically face multiple layers of deductions, including factory development levies, management fees, brokerage and auction costs, and county-level cess charges. In aggregate, these deductions significantly compress the share of export value accruing to farmers, despite tea being a leading foreign exchange earner for the economy.

In contrast, Uganda’s tea sector operates under a comparatively lighter fiscal regime, with no dedicated export tax or sector-specific levies applied to tea, potentially positioning it as a lower-cost competitor and, in some export segments, allowing it to eclipse Kenya on price competitiveness where quality differentials are less pronounced.

In this instance, the tea sector could therefore benefit from a calibrated reduction or rationalisation of tea-related taxes and levies, alongside broader fiscal and logistics interventions, to cushion farmers from prevailing economic pressures.

Kenya’s fiscal responsiveness to global shocks, as already demonstrated in fuel-related interventions, provides a useful precedent for extending similar stabilisation logic to key agricultural and export value chains. Strengthening these safeguards will be essential to sustaining export performance, stabilising rural livelihoods and advancing Kenya’s broader economic transformation agenda.