From Flat Fees to Revenue-Based Licensing: What the Proposed Banking Reforms Mean for Banks

For the first time in more than three decades, Kenya is proposing a fundamental change to how commercial banks pay for their operating licences.

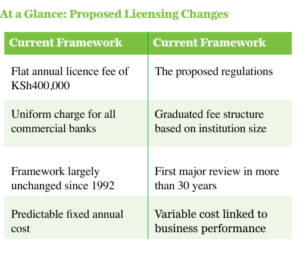

The Central Bank of Kenya (CBK) has proposed replacing the long-standing flat annual licence fee with a graduated framework based on a bank’s gross annual revenue. While the proposal aims to modernise a licensing structure that has remained largely unchanged since 1992, it also introduces new operational and financial considerations for banks, particularly larger institutions.

In the past, all commercial banks paid the same annual fee. The new proposal would charge banks different amounts depending on their size. This change reflects the increasing complexity of Kenya’s banking sector. Still, it raises questions about how it will be implemented, how banks will budget for it, and what the total regulatory cost will be.

What Is Changing?

For more than 30 years, commercial banks have operated under a uniform licensing structure, paying an annual licence fee of KSh400,000 irrespective of their size or revenue.

The proposed regulations replace that approach with a graduated model based on annual gross revenue. Under the new framework, larger institutions would pay significantly higher licence fees than smaller banks. At the same time, mortgage finance companies, digital credit providers and representative offices would also be subject to revised fee structures.

Although the proposal represents an administrative change, it effectively introduces a recurring operational cost that will vary with business performance.

More Than a Licensing Fee

Viewed in isolation, the revised licence fees may appear modest compared with the revenues generated by Kenya’s largest banks. However, financial institutions are increasingly operating in an environment of expanding regulatory obligations. Investments in cybersecurity, anti-money laundering compliance, data protection, consumer protection, environmental and social risk management, operational resilience and digital infrastructure have all increased the cost of doing business.

Against this backdrop, the proposed licensing reforms are another component of a broader compliance landscape rather than a standalone fee adjustment. For banks, the issue is therefore less about the absolute value of the licence fee and more about the cumulative impact of multiple regulatory requirements on operating expenditure.

Planning for Higher Operating Costs

One of the first effects of the proposal will be on financial planning. Since licence fees will depend on annual revenue, banks will have to include a changing regulatory cost in their budgets. Unlike the old fixed-fee system, future licensing costs will rise or fall as the business grows.

For expanding banks, particularly those pursuing aggressive growth strategies or regional expansion, stronger financial performance could also lead to higher annual licensing obligations.

While this aligns with the principle that larger institutions should contribute more towards regulatory oversight, it also introduces an additional operational consideration that did not previously exist.

Implications for Competition

The reforms may also have different effects across the banking sector.

Large banks are expected to incur the largest increase in licensing costs, reflecting both their revenue base and the complexity of supervising systemically important institutions.

Smaller banks, meanwhile, may face comparatively lower financial obligations under the graduated structure.

For new market entrants, regulatory costs remain one of several factors considered when assessing expansion into Kenya’s banking sector.

Although the proposal is unlikely to alter competitive dynamics on its own, it is part of a broader regulatory environment in which institutions continue to balance compliance investments with digital transformation, customer acquisition, and operational efficiency.

A Modern Framework, with a Phased Transition

Few would argue that Kenya’s banking sector looks the same as it did in 1992. Over the past three decades, the industry has evolved into one of Africa’s most sophisticated financial markets, driven by digital banking, mobile financial services, regional expansion and increasingly complex financial products.

Updating a licensing framework that has remained unchanged for more than 30 years is therefore understandable. Recognising the significance of the reforms, the Central Bank of Kenya has proposed a four-year transition period to allow institutions to adjust gradually to the new licensing regime, rather than implementing the full changes immediately.

Under the new plan, commercial banks would pay 0.13% of their gross annual revenue in 2026, 0.14% in 2027, and 0.15% from 2028 onwards. The licence fee will be based on each bank’s audited and published financial statements for the previous year, ensuring consistency in the calculation.

The regulations also recognise the unique position of newly licensed institutions. Banks that have not yet commenced operations will have their licence fees assessed based on their projected average gross annual revenue for the first three years of business. This approach enables new entrants to meet regulatory requirements while acknowledging that they do not yet have an established financial history.

From an operational perspective, these proposals add further compliance steps. Banks must pay the annual licence fee to the Central Bank in a single payment within the specified time. If they don’t pay within 90 days, they will be fined double the annual fee. If they continue to fail to pay, they could face more serious actions, including possibly losing their licence under the Banking Act.

While the phased implementation gives institutions time to adapt, banks will still need to incorporate the revised licensing framework into their medium-term financial planning, budgeting and regulatory compliance strategies as the new regime is gradually introduced.

Looking Ahead

The proposed reforms are unlikely to change customers’ day-to-day banking experience. However, they represent another step in the ongoing evolution of Kenya’s regulatory landscape.

For banks, the proposal is less about a single increase in licence fees than about operating in an environment where regulatory expectations continue to rise alongside the industry’s growth and complexity.

As the proposals progress through the public participation process, the conversation is likely to extend beyond the fees themselves. It will focus on ensuring that the framework achieves its intended regulatory objectives while remaining predictable, proportionate and supportive of a competitive banking sector.