INTERPOL Fraud Threat Report Signals a New Era of Global Financial Crime

The release of INTERPOL’s latest global threat assessment offers a sobering reminder that financial fraud is no longer a peripheral criminal activity. The second edition of the Global Financial Fraud Threat Assessment presents a picture of a rapidly evolving threat landscape in which technology, globalisation, organised crime networks, and weak regulatory environments are converging to create unprecedented risks for individuals, businesses, and governments. The report does more than catalogue criminal trends. It signals a structural shift in the nature of financial crime, one that carries significant implications for policymakers, financial institutions, and corporate actors across emerging and developed markets alike.

INTERPOL’s Global Financial Fraud Threat Assessment is designed as a forward-looking review of patterns observed by law enforcement agencies across its member countries. The 2025 edition builds on findings published in 2024, reflecting a period in which financial crime has accelerated in both scale and sophistication. Unlike traditional crime reports that focus on isolated cases, the assessment aggregates intelligence from multiple jurisdictions to identify systemic risks, emerging techniques, and the level of preparedness among enforcement authorities.

The timing of the report is notable. Digital financial services have expanded rapidly across the world, driven by mobile money, online banking, cryptocurrencies, and cross-border payment platforms. The same technological environment that has enabled financial inclusion has also lowered the barriers to entry for criminal activity. Fraud schemes that once required physical presence can now be conducted remotely, often across several jurisdictions simultaneously, complicating investigation and prosecution.

Key Findings: Scale, Sophistication, and Global Reach

One of the most striking conclusions in the report is the sheer scale of financial fraud. Global losses linked to financial fraud in 2025 alone are estimated at $442 billion, placing it among the most costly forms of transnational crime. INTERPOL assesses the overall global risk posed by financial fraud as high, with expectations that the scale of offending will grow significantly over the next three to five years.

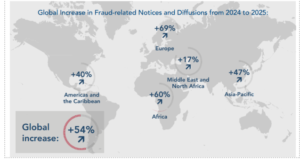

Law enforcement cooperation has improved, though the rise in fraud cases has outpaced enforcement capacity. Since 2024, the number of fraud-related Notices and Diffusions issued through INTERPOL channels has increased by 54 per cent, with European member countries accounting for the majority. During the same period, the organisation supported more than 1,500 transnational fraud investigations involving lost assets valued at approximately $1.1 billion. These figures illustrate both stronger collaboration and the growing complexity of cases being handled.

The report also highlights the global spread of scam centres, which have evolved from a regional phenomenon into a worldwide criminal infrastructure. Facilities linked to online fraud operations have been identified across multiple regions, employing hundreds of thousands of individuals. Many of those involved are themselves victims of human trafficking, forced to carry out online scams targeting people in other countries. Victims from nearly 80 countries have been trafficked into such centres, demonstrating the truly transnational character of the threat.

Technology is emerging as the defining factor in the next phase of financial fraud. Artificial intelligence tools available on illicit marketplaces can now generate convincing voice and video clones using only seconds of authentic recordings. Criminal groups are using these capabilities to impersonate relatives, colleagues, public figures, or business executives in order to manipulate victims into transferring funds. The report also points to the rise of so-called agentic AI, capable of autonomously planning and executing fraud campaigns, from identifying targets to sending messages and coordinating payment requests. AI-enabled fraud is increasingly linked to investment scams, impersonation schemes, sextortion, and fake kidnapping cases.

Another major concern is the growing level of organization among criminal networks. Fraud groups are operating more like businesses, specializing in different stages of the crime cycle. Some groups focus on data harvesting, others on social engineering, while separate networks handle money laundering through complex international channels. This specialization allows fraud operations to scale rapidly and to adapt quickly when law enforcement tactics change.

Implications for Africa and the Global Financial System

The report carries particular significance for the African region, where financial fraud is increasingly intersecting with broader security risks. INTERPOL notes an expanding nexus between fraud schemes and terrorist financing, with extremist groups using online scams and crypto-based fraud to generate resources. This trend raises concerns that financial crime is not only an economic threat but also a driver of instability in vulnerable regions.

For governments, the findings underline the need for stronger regulatory coordination, improved digital forensic capacity, and tighter oversight of emerging financial technologies. Financial institutions face growing pressure to invest in fraud detection systems capable of responding to AI-driven threats. Corporates operating across borders must recognize that fraud risk is no longer confined to internal controls or customer verification processes. Exposure now extends to supply chains, digital platforms, and even employee communications.

INTERPOL’s assessment ultimately points to a future in which financial fraud becomes more automated, more global, and more difficult to trace. The report therefore serves as a warning that the fight against financial crime will depend not only on law enforcement, but on sustained cooperation between regulators, businesses, and international institutions. Failure to respond at the same pace as criminal innovation could allow financial fraud to become one of the defining economic risks of the digital age.